You might have heard the phrase “timing the market” before.

If you haven’t, it’s a strategy used by active investors or traders aiming to increase their investment returns by predicting and profiting from market downturns and uplifts.

Timing the market is an exciting prospect, but notoriously difficult to accomplish, as predictions are based on probabilistic, educated guesses.

Instead, a strategy focused on “time in the market” can produce better results by emphasising stable long-term growth over short-term high-risk gains.

Keep reading to learn why the nature of the stock market makes timing the market so difficult, and how long-term investing can help you build wealth more reliably.

Markets are impossible to predict, which makes timing difficult to execute successfully

Timing the market involves predicting exactly when to move in and out of the stock market to take advantage of market volatility.

Specifically, investors sell investments before prices fall to mitigate their losses and buy them back before they rise to maximise profit.

For example, if you had sold investments in the FTSE All-Share Index when President Trump announced his reciprocal tariffs on 2 April 2025, you might have avoided market losses of 10.85%. If you then repurchased these equities on 9 April 2025, you could have benefited from 14.91% investment growth up to 12 June 2025 – based on London Stock Exchange (LSE) data.

However, to achieve these returns, you would have had to exit and buy back into the market at the right time. This is incredibly difficult because market movements are impossible to predict with 100% accuracy as they are influenced by a myriad of factors, including:

- Supply and demand

- Inflation

- Interest rates

- Geopolitical events

- Tax increases

- Market sentiment

Predicting which way the market will move is largely based on identifying short-term probabilities and then acting on them based on intuition and gut feeling.

This isn’t impossible – day traders have made careers from timing the market using analytical and algorithmic tools. However, it’s incredibly rare to time the market both successfully and consistently.

Active investing also requires extensive monitoring of market movements, current events, and economic forecasts, which isn’t feasible for anyone who isn’t a full-time investor.

“Timing the market” is a high-risk, investment strategy

While you may get lucky and time the market perfectly, what often happens instead is that investors miss out on valuable growth when stock values rebound.

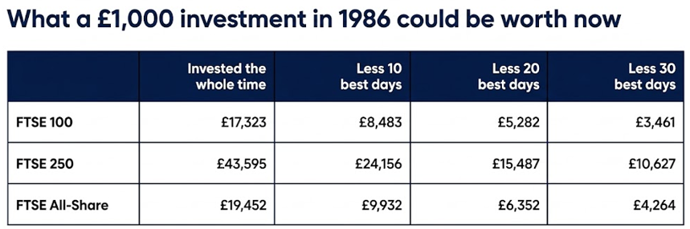

In fact, Schroders found that missing out on just 10 of the best-performing days in the FTSE 100 Index over a period of 35 years would have turned £1,000 into £8,483 (between January 1986 and January 2021).

Source: Schroders

For comparison, if you had stayed invested the entire time, your £1,000 would have grown to £17,323.

“Time in the market” prioritises long-term investing to build lasting wealth

On the opposite side of the spectrum, time in the market, or “buy-to-hold” strategies, emphasise holding investments over a long period of time, despite any short-term dips.

Rather than beating the market, this method relies on holding investments long enough for markets to recover and continue growing.

Historical data shows that markets tend to trend upwards over long periods of time. The FTSE All-Share Index, for example, has produced total returns of 1,274.79% since its inception on 10 April 1962 up to 10 April 2026, according to LSE data. This is a 64-year investment time frame, which can be the time frame of many pension investors, assuming pension savings start at 20 and continue to age 84

While past events like the dotcom bubble and the 2008 financial crash caused stock markets to dip, history shows us that they eventually recovered. Ultimately, investors would have been better off holding on to their investments rather than selling.

However, while it’s important to learn from history, remember that past performance isn’t a reliable indicator of future events.

There is more opportunity to spread risk in long-term investing to increase your likelihood of positive returns

Investment risk is unavoidable. But unlike timing the market, where risk is perpetually high, you have the opportunity to manage it when investing for the long term. Crucially, you may want to think in decades, not days; this is the approach taken by some of history’s greatest investors.

Alongside holding investments for extended periods, there are two main strategies for mitigating long-term investment risk.

Diversification

When investing, one of the key ways to manage risk is through diversification. A diversified portfolio spreads your money across a range of investments, different asset classes, and various geographical regions.

In the short term, markets can be unpredictable and individual investments may rise or fall sharply. Diversification helps reduce the impact of this short‑term volatility, as weaker performance in one area may be offset by stronger returns elsewhere over time.

Pound cost averaging

Pound cost averaging involves investing a fixed amount regularly.

Rather than investing a large lump sum all at once, pound cost averaging helps you spread purchases, buying fewer units when markets are high and more when markets are low.

This reduces the impact of market volatility: when markets fall, your fixed investment account automatically purchases more units, which lowers your average cost per unit.

Over time, the price you pay for your investments tends to average out, protecting you against market fluctuation.

Learn more about pound cost averaging by reading: How regular investing could help you balance risk through “pound cost averaging”

Get in touch

A long-term investment strategy is a vital pillar of any financial plan. If you’d like to discuss your options, then please contact us.

You can email enquiries@rfsl.co.uk to book an appointment with your adviser today. Alternatively, call 01534 502000 in Jersey or 01481 747940 in Guernsey to set up a meeting.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Rossborough Financial Services Limited is regulated by the Jersey Financial Services Commission under the Financial Services (Jersey) Law 1998 and licensed by the Guernsey Financial Services Commission.